Subsea cables are the hidden infrastructure of the internet. They are fiber-optic systems laid across seabeds, carrying around 98 percent of international internet traffic between continents, then coming ashore at cable landing stations where “wet” undersea systems connect to “dry” terrestrial networks, or national internet networks.

But they are more than pipes. They are also routes, jurisdictions, contracts, landing stations, repair dependencies, and bargaining power.”A country that owns a cable, or holds a meaningful stake in one, controls where its data flows, who can access it in transit, and whether it can be used as leverage in trade, security, or diplomatic negotiations.

On January 15, 2026, Maharat reported that the Lebanese Cabinet approved the Ministry of Telecommunications’ request to join the Medusa International Submarine Cable Project.

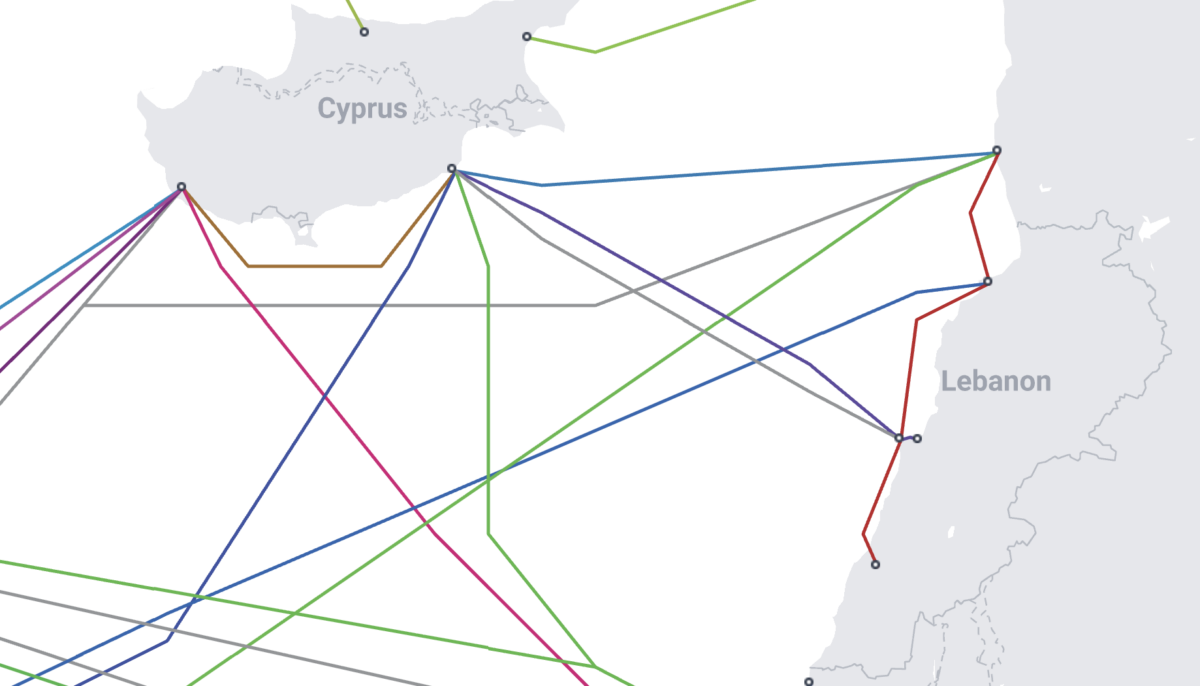

Medusa is a high-capacity Mediterranean system owned by AFR-IX Telecom and backed by EU support, designed to connect Europe, North Africa and the Eastern Mediterranean. The core system spans 7,100 km and was expected to be operational between 2025 and early 2026, with planned extensions toward the Middle East and Africa bringing the total route to approximately 8,700 km, enough to carry the equivalent of millions of simultaneous video streams (EIB, European Commission, Medusa SCS). Its official site lists landing points including Marseille (France), Mazara (Italy), Yeroskipou (Cyprus), Tartous (Syria), Port Said (Egypt), and Aqaba (Jordan), but not Lebanon.

Lebanon joined a cable that does not land on its territory. Participation without a landing point is access, not sovereignty. Worse, Lebanon has barely treated subsea connectivity as a matter of national security or cybersecurity strategy. Israel, Cyprus, Greece, Gulf states, and now Syria are positioning themselves as corridors between the Gulf and Europe. Lebanon is treating cables as connectivity procurement.

This is why the Lebanese cable debate needs a different frame. The question is not only whether the internet can be cut during war, or whether one cable creates vulnerability. The deeper issue is digital sovereignty: does Lebanon have strategic choices over where its data moves? Who controls the infrastructure it depends on? How much leverage does it hold as regional routes are redrawn—and what risks does this pose?

What does it mean to own a submarine cable?

Ownership of a submarine cable is a spectrum of distinct rights and obligations that vary depending on how a party participates in the system. The table below summarises the key forms of participation and what each confers in practice.

Table 1: Cable ownership — rights conferred and obligations assumed

| Ownership form | What it confers | Key obligations |

| Sole ownership | Full control over construction contracting, routing decisions, landing‑point selection, maintenance scheduling, and capacity allocation | Sole responsibility for all permits, landing licences, supply contracts, and maintenance costs |

| Consortium / Joint ownership (via Construction & Maintenance Agreement, C&MA) | Pro‑rata share of fiber pairs; voting rights on project decisions; access to the cable’s landing points proportional to investment | Capital contributions; shared maintenance costs; consent obligations before a change of control |

| Landing party status | Right (and obligation) to land the cable on national territory; access to the cable at the national landing station; ability to levy transit and landing fees | Must hold national telecommunications licence and landing permits; responsible for terrestrial segment within national borders |

| IRU (Indefeasible Right of Use) | Exclusive, long-term right (typically 20–30 years) to use a defined amount of capacity on another party’s cable; the right cannot be revoked, and can be sold to others or treated as a financial asset. | No rights over the physical cable itself; no voting rights in consortium decisions; maintenance costs shared via the C&MA |

| Cable builder / supplier | Controls physical construction, routing decisions during laying, and the technical architecture of the system | Contractual delivery obligations; warranty and repair |

So the sovereignty question is concrete: is Lebanon joining Medusa as a partner with control, landing rights and route leverage, or mainly buying capacity from a system designed elsewhere? Applied to Lebanon’s portfolio, the answer is not straightforward. Across its cable portfolio, Lebanon’s pattern of participation and ownership exposes a gap between formal involvement and strategic control. Medusa is the latest iteration, as Beirut is not yet stated as a landing point.

IMEWE carries the bulk of Lebanon’s connection. Through OGERO, Lebanon holds approximately 12 percent of the system—a meaningful consortium stake in a roughly 13,000 km India–Europe route with multiple landing points between Mumbai and Marseille.

Alexandros is similar. Lebanese authorities reported purchasing a 25 percent share in the Cyta-owned Alexandros subsystem of TE North, valued at over $20 million in 2013. This increased Lebanon’s share of Alexandros capacity from 310 Gbps to 1,920 Gbps, meaning faster connection speeds and greater capacity to handle traffic without bottlenecks, on a system that physically lands in Cyprus, Egypt and France, with Beirut accessing it via Cypriot infrastructure rather than as a direct landing party.

BERYTAR is another example, it was established in 1997 as a bilateral cable linking Lebanon and Syria with no consortium structure or landing complexity.

CADMOS‑2,which replaced the CADMOS cable system interconnecting Lebanon and Cyprus since 1995, is the exception. The state co‑signed and co‑built a bilateral link of roughly 230 km between Beirut and Pentaskhinos. It is the closest thing in Lebanon’s cable portfolio to genuine co-ownership of a physical system.But for Cypriot operators, CADMOS‑2 is a new subsea connection that reinforces Cyta’s role as a telecommunications hub and “digital gateway” between Europe and the Middle East.

Table 2: Lebanese subsea cable ownership overview

Three vulnerabilities follow from this picture.

First: the security problem. Lebanon’s international connectivity depends on foreign landing points, foreign-controlled systems and politically sensitive routes. That does not prove interception or sabotage. But exposure is structural.

In modern conflicts, cables, clouds, metadata, data centers and landing stations form part of the same strategic surface.

The Cradle argues that digital modernization without data governance, sovereign encryption, multi-vendor strategy, and safeguards can deepen asymmetry rather than strengthen sovereignty.

Second: the traffic problem. Connectivity is power because traffic creates dependency and revenue. If Gulf-to-Europe data flows through Israel, Syria, Egypt, Cyprus or Greece, those states become more than transit points; they become unavoidable nodes.

A Times of Israel blog framed this bluntly as a “cable war” Israel is at risk of losing if Syria becomes a credible Saudi route to Europe. Data Center Dynamics reported that STC Group won a bid to run Syria’s SilkLink project, acquiring a 75 percent stake, with a total investment of $800 million, covering a 4,500 km fiber-optic network, data centers, submarine landing stations and regional links with Jordan, Lebanon and Turkey. Middle East Eye and The Cradle reported that Saudi Arabia wants to route an East-to-Med data corridor through Syria rather than Israel.

Third: the physical-control problem. “Owning a cable” can mean very different things. Equity in a system is not the same as buying capacity. A landing station is not the same as the wet segment. A small consortium stake is not the same as being the anchor tenant that shapes upgrades, routes and expansion.

Alexandros illustrates the ambiguity: Lebanese reporting says the ministry bought a 25 percent share, while system sources describe Alexandros as Cyta-owned infrastructure implemented through TE North and not as a Lebanon landing system (Submarine Networks).

This is why Medusa cannot be discussed only as an emergency internet backup. It may be necessary. Lebanon’s older CADMOS system has reached the end of its assumed life, and Maharat notes that IMEWE also has a limited remaining lifespan .

But necessity is not strategy. If Lebanon joins Medusa without clarifying whether it owns capacity, fiber pairs, landing rights, upgrade rights or only service access, it may gain resilience while staying outside the corridor game.

CADMOS-2 raises the same structural question: it deepens Lebanon’s reliance on Pentaskhinos, a landing site embedded in Cyprus’s broader role as an Eastern Mediterranean cable and infrastructure hub. The same Pentaskhinos landing point also serves the Israeli–European MedNautilus system, a submarine cable connecting Italy, Greece, Turkey, Cyprus and Israel.

Concentrating both CADMOS/CADMOS‑2 and MedNautilus at Pentaskhinos does not automatically constitute a vulnerability, but it does sharpen a national security dilemma: Lebanon’s principal international gateway is increasingly routed through infrastructure that is tightly integrated into Israeli–European traffic and controlled from outside Lebanese jurisdiction.

The minimum strategy is clear. Lebanon should map cable assets, landing points, capacity rights, contracts and dependencies. It should clarify what the state owns, what OGERO operates, what private actors control, and what foreign partners provide.

Lebanon should treat cables as matters of national security, economic planning and foreign policy and decide whether it wants to be a Mediterranean spur, a redundant access market, or a deliberate node linking Cyprus, Syria, the Gulf and Europe.

The region’s new map will not be drawn by speeches about sovereignty. It will be drawn by cables, landing stations, routes and contracts. Lebanon can keep buying access to maps designed by others, or it can decide where it wants to sit on them.

Featured image from https://www.submarinecablemap.com/